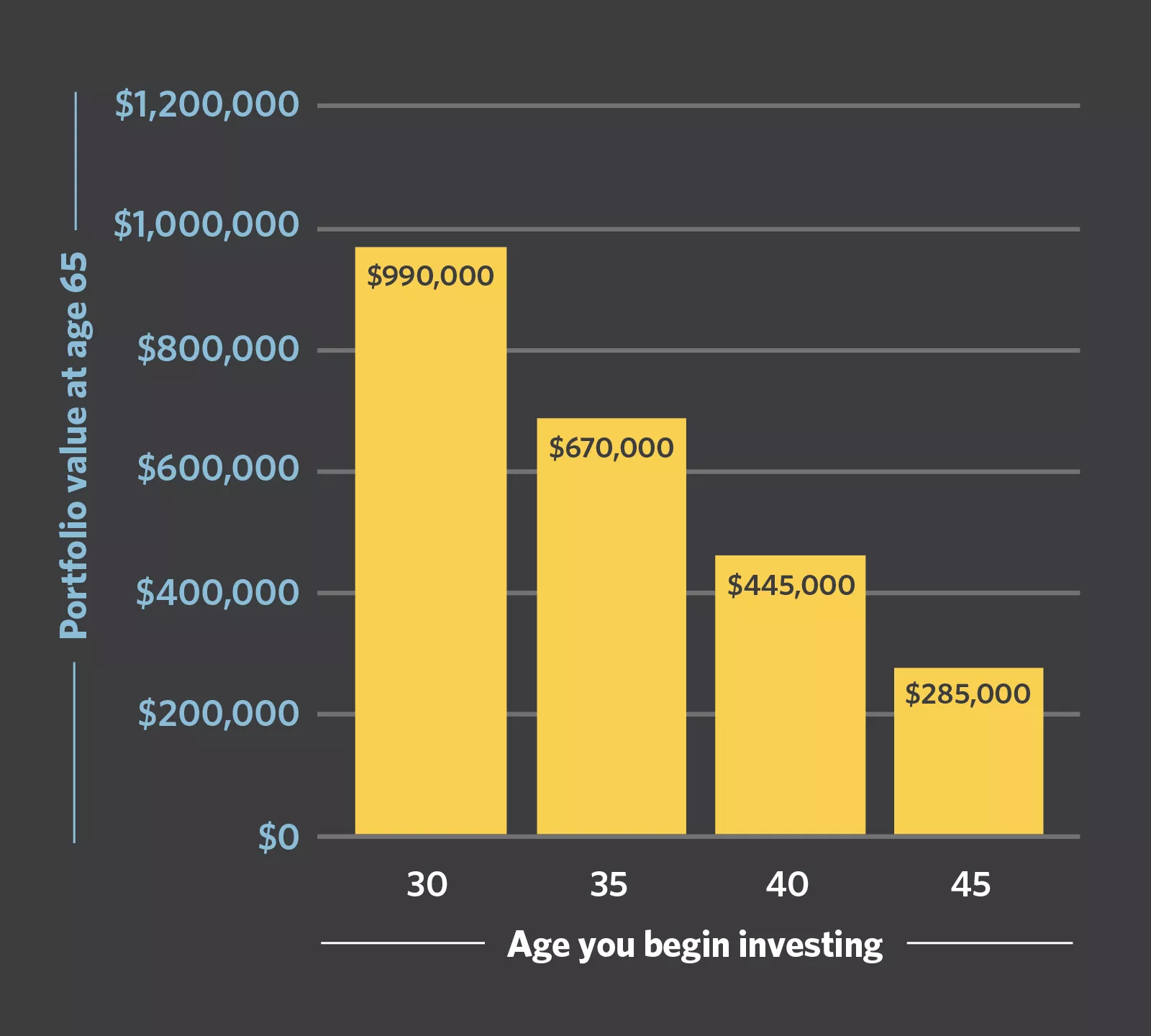

This bar chart shows that waiting a decade to begin saving can significantly decrease the amount of money you'll have when you're ready to retire. The tallest bar shows that you could have a portfolio valued at $1,255,000 by age 65 if you started investing $550 per month with a 7% hypothetical annual return at age 25. The next tallest bar shows that you could have a portfolio valued at $610,000 by age 65 if you invested the same amount at the same return starting at age 35. The last bar shows that you could have a portfolio valued at $275,000 by age 65 if you invested the same amount at the same return starting at age 45. This example doesn't include taxes, fees and commissions, which would reduce the return. Figures are rounded to the nearest $5,000.

Investing in your 20s

You've graduated from school and have joined the working world. Congratulations! To help you make the most of your paycheques, here are a few simple tips.

Since time is on your side, building good financial habits in your twenties can lead to greater financial satisfaction in your future.

Create a budget

A budget can help you stay on track with your savings goals. You'll want to begin by adding up the income you make. Then subtract your expenses, which include any debt you have as well as rent, utilities, your car payment, etc. Using the remainder, you can put together a plan of what to do with the money you have left. You can also determine if you need to/want to cut expenses, which could be done by packing a lunch, living with roommates or your parents, or picking up additional work on the side.

Manage debt

Having too much debt can hurt your credit score and interfere with you achieving your financial goals. If you're able to, consider paying extra on your debt, and more than the minimum payment on credit cards. Even better, pay off your credit card bill every month.

Contribute to your company's retirement plan

When you've just started working, retirement sounds years away. While it is, you should take advantage of the fact that time is on your side by beginning to save now. Many companies match retirement plan contributions, which is free money you shouldn't pass up. And as you can see from the chart below, waiting just a few years to begin saving can significantly decrease the amount of money you'll have when you're ready to retire.

Create a financial strategy to save and invest

It's important to note the difference between saving versus investing. Saving is putting money aside in a low, fixed interest rate savings or money market account, perhaps for an emergency. It's just one part of your financial strategy. Investing is using your money to potentially create more money over a period of time. While investing can carry risk, not investing can also be a risk to your financial future. Whether you invest in your company's plan or outside of it, it's important to get started as soon as possible.

Consider working with a financial advisor

A financial advisor can help you manage your money. He or she will work with you to understand your investing goals and investing style. While you might be doing research on your own, working with a financial advisor can help you understand the broader picture. Together, you'll be able to develop a plan to help you achieve those goals.

Learn how we can help you get and stay on the right financial path. Give us a call today.

Katherine Tierney

Katherine Tierney is a Senior Retirement Strategist on the Client Needs Research team at Edward Jones. The Client Needs Research team develops and communicates advice and guidance for client needs, including retirement, education, preparing for the unexpected and leaving a legacy. Katherine has more than 15 years of financial services and retirement experience. She is a contributor to Edward Jones Perspectives and has been quoted in various publications.